On April 17, the National Automobile Dealers Association (NADA) hosted a webinar with senior staff from the Federal Trade Commission (FTC) to clarify enforcement expectations following the agency’s March 13 warning letters to 97 dealerships nationwide.

Although the webinar addressed a wide range of advertising practices, the discussion consistently returned to the issue most relevant to Minnesota dealers: what the FTC’s position means for document fees (“doc fees”) in advertised vehicle prices. The FTC made clear that dealers in all 50 states must include the doc fee in the most prominent advertised price (the “all-in price”). The FTC’s treatment of doc fees illustrates a broader enforcement priority: ensuring that the most prominent advertised price reflects all non-government fees that a consumer must pay to purchase the vehicle.

FTC Authority: Section 5 and the Enforcement of “All-In Pricing”

The FTC does not rely on a new rule or regulation to enforce its position. Instead, it applies Section 5 of the Federal Trade Commission Act, which prohibits unfair or deceptive acts or practices in commerce. The FTC explained that Section 5 gives it authority to challenge advertising that materially misleads consumers or fails to clearly and conspicuously disclose material terms.

The FTC evaluates advertisements from the perspective of a reasonable consumer. Under this standard, an advertisement becomes deceptive if a consumer cannot purchase a vehicle for the advertised price plus only taxes, title, and registration. The FTC has made clear that excluding mandatory dealer fees, including doc fees, is illegal under Section 5 of the FTC Act.

The Core Rule: What Must Appear in the Advertised Price

The FTC reiterated that the most prominent advertised price must reflect the total price available to all consumers (more guidance on prominence can be found on page 17 of the FTC’s dotcom disclosure guidelines). A consumer must be able to walk into the dealership and purchase the vehicle at that price, plus only government fees. A dealer cannot satisfy this standard by:

- Omitting a price entirely

- Advertising a base price that excludes mandatory non-government fees

- Relying on disclaimers or fine print to correct a misleading headline price

The same principles apply to lease advertising. A consumer must be able to obtain the advertised monthly payment or complete the lease for the advertised amount due at signing, plus only government charges. Mandatory fees, including doc fees, must be included in the advertised payment or due-at-signing amount, depending on how the fee is structured.

The FTC emphasized that prominence matters. The all-in price must dominate the advertisement, while additional disclosures must appear less prominently and must not create confusion.

The FTC also confirmed that dealers may advertise MSRP, but only if it appears less prominently than the all-in advertised price.

Doc Fees: Central to the FTC’s Pricing Standard

The FTC used doc fees as the clearest example of its enforcement position. The FTC confirmed that dealers must include doc fees in the advertised price in all 50 states.

- Government charges, such as taxes, title, and registration, which may be excluded from the total advertised (most prominent) price

- Non-government fees, such as doc fees, which must be included in the total advertised (most prominent) price

The FTC distinguishes between fees required by a government authority and fees that are merely authorized by state law. Government charges are limited to amounts the dealer must collect and remit directly to a government entity, such as taxes, title, and registration.

Fees like the doc fee, even if permitted or authorized under state law, are not treated as government charges because they are imposed by the dealer, retained by the dealer, and not required to be paid to a government authority. As a result, the FTC classifies doc fees as de

aler-imposed charges that must be included in the most prominent advertised price. The FTC does not regulate the amount of the doc fee; it regulates how the fee is presented in advertising to ensure it is included in the all-in price.

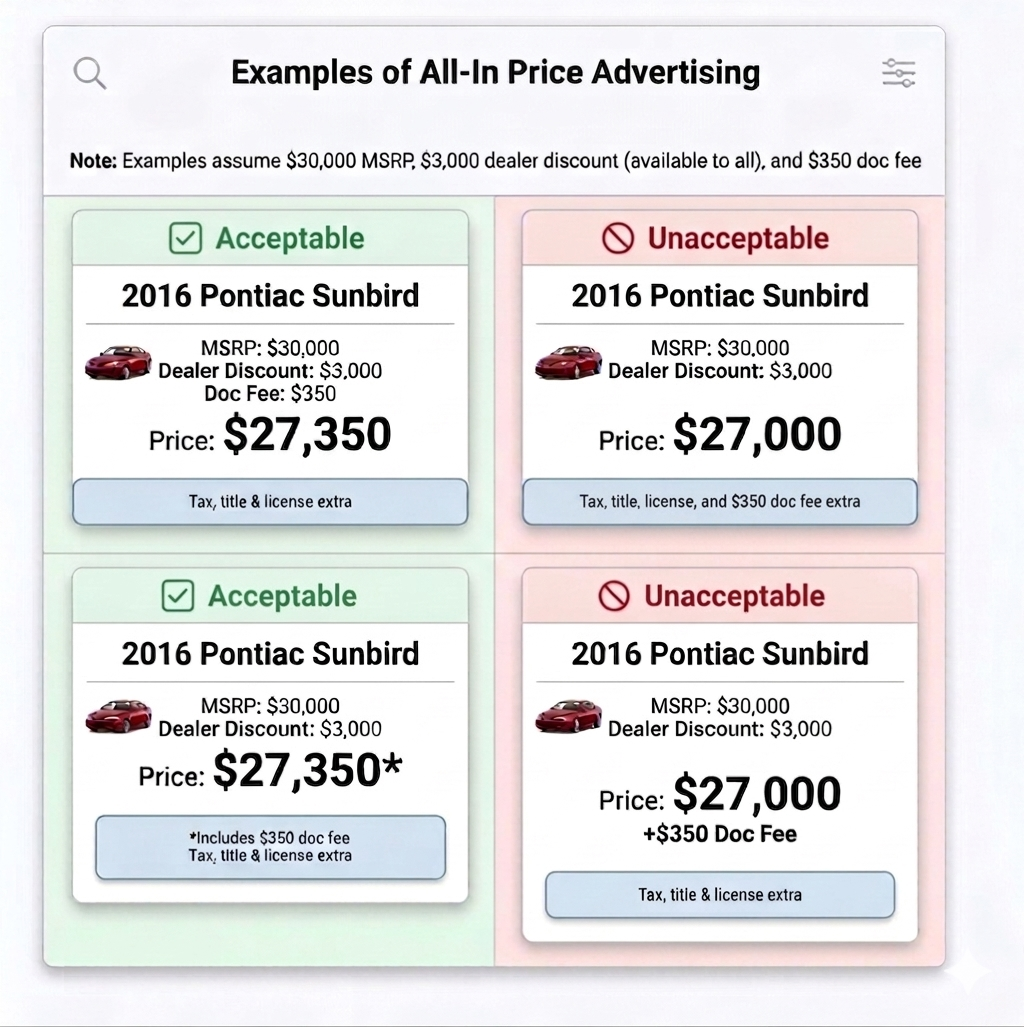

Dealers may still itemize the doc fee separately, but they must include it in the most prominent advertised price. The following examples show how dealers should treat the doc fee in advertisements:

Other Mandatory Pricing Components

The FTC applies the same standard to any fee required to complete the transaction. If a consumer cannot decline the charge and still purchase the vehicle, the dealer must include it in the most prominent advertised price. This includes:

- Freight or destination charges

- Dealer preparation or handling fees

- Additional dealer profit or margin

The FTC focuses on economic reality rather than labeling. Renaming a charge does not change its treatment if the consumer must pay it to complete the purchase.

In-Transit and Availability of Vehicles

The FTC addressed advertising for in-transit and otherwise unavailable vehicles and emphasized that dealers must ensure consumers have a reasonable expectation that the vehicle can be purchased. Dealers may advertise in-transit vehicles if they clearly disclose the status of the vehicle and if the vehicle is expected to arrive within days (1 to 2 days), rather than weeks. The FTC cautioned that advertisements should not present vehicles as available for immediate purchase if they are not realistically obtainable at the time of the advertisement. If a vehicle becomes unavailable, the dealer should remove or promptly update the advertisement to avoid misleading consumers under Section 5 of the FTC Act.

Truly Optional Fees

The FTC permits dealers to exclude optional products and services from the most prominent advertised price only when those products are genuinely optional and clearly disclosed as such. A fee is optional only if:

- The consumer clearly understands it is not required

- The consumer can decline it without affecting the vehicle purchase price

- The dealer clearly and conspicuously discloses that choice

Optional status cannot depend on fine print or buried disclaimers. The FTC evaluates whether a reasonable consumer would understand the charge as optional at the time of the advertisement. The following examples illustrate how that standard applies in practice:

Example #1: EVTR Fee

Minnesota law requires dealers to list the EVTR fee as optional on the purchase agreement (it must appear as “optional electronic transfer fee”). If the dealer allows the customer to complete the titling process through traditional means and does not condition the transaction on the use of EVTR, the dealer may treat the fee as optional. In that circumstance, the dealer need not include the EVTR fee in the most prominent advertised price.

Example #2: Optional Add-Ons

The FTC stated that optional products may be excluded from the all-in price if clearly disclosed. Items such as window tint or flashing brake lights may qualify if the consumer can decline them without affecting the vehicle purchase price. In assessing optionality, the FTC may also consider whether the add-on is easily removable or reversible and whether consumers actually opt in at meaningful rates, as low uptake can indicate that the product is not functionally required to complete the transaction. However, products such as undercoating, rustproofing, or clearcoat are typically not optional once applied and therefore must be included in the all-in price if required for purchase.

Example #3: Credit Card Surcharges

A credit card surcharge may be excluded from the all-in price if the dealer offers a genuine and clearly disclosed alternative payment method—such as cash, check, or ACH—without additional charge.

Advertising Scope and Dealer Responsibility

The FTC defines advertising broadly. It includes:

- Dealer websites and vehicle detail pages

- Third-party listing platforms

- Social media and paid search advertising

- Radio, television, and direct mail

- Oral representations made on the lot

The FTC emphasized that dealers remain responsible for advertising they control. While OEMs and third-party platforms may influence content, responsibility attaches to the entity that controls the advertisement.

Enforcement Outlook and Compliance Risk

The FTC stated that it intends to aggressively pursue dealers that do not comply with Section 5 standards. Dealers face potential civil penalties of up to $50,120 per violation or per day for ongoing violations where applicable. The FTC may also pursue injunctive relief, consent orders, and ongoing compliance monitoring.

The FTC’s enforcement action against Lindsay Auto Group illustrates this risk. The FTC alleged that Lindsay deceived consumers for years by advertising falsely low prices and including unwanted add-ons that resulted in buyers paying thousands of dollars more for their vehicles. The agency secured a $75 million settlement that included monetary relief and imposed extensive compliance obligations governing future advertising practices.

The FTC’s warning letters and webinar guidance indicate that additional enforcement activity is likely.

Purchase Agreements Remain Unchanged

The FTC’s guidance applies to advertising only and does not alter Minnesota purchase agreement requirements. Dealers must continue to itemize all fees and taxes, including doc fees, in the transaction documents. Dealers are expected to advertise an all-in price that includes mandatory non-government fees while separately itemizing those fees on the purchase agreement. The two requirements operate independently.

Next Steps: FAQs and Industry Guidance

The FTC confirmed that it will issue additional FAQs to provide further clarification on advertising requirements under Section 5. MADA is working with its Ad Standards Steering Committee to evaluate and update its Advertising Standards in response to the FTC’s guidance. MADA will continue to monitor enforcement activity and provide updates as additional guidance becomes available.